A new HSBC report suggests that if and when Quantitative Easing is being reversed it could be a watershed event for sectoral equity performance. Their view is based on the concept of “equity duration”. The long-standing outperformance of low-beta and high-quality stocks, which have longest duration and benefited most from three decades of falling yields, should come to an end and be replaced by relative strength of cyclical, financial and materials stocks.

“How to survive the end of QE” HSBC Equity Insights, 21 March 2013,

Peter Sullivan, Robert Parkes and Garry Evans

“High quality and low beta stocks have performed strongly for many years and could be in for a huge shock…These styles are long duration and have ridden the wave of falling bond yields (down 90% in the US since 1981). They are likely to be among the most vulnerable when QE ends…Short duration sectors such as cyclicals and financials are well placed to outperform when bond yields rise and consumer staples and healthcare are most at risk…the materials sector is low duration and performs consistently well when bond yields rise, and it doesn’t matter whether it’s real growth or inflation that is driving bond yields higher.”

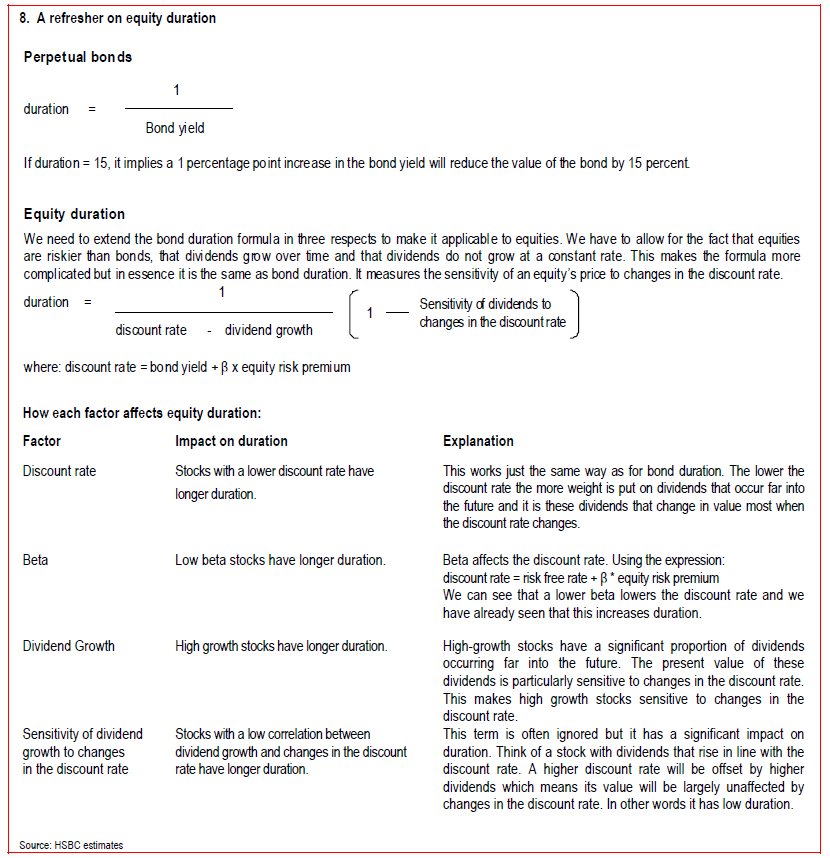

“If we want to think about the average time over which dividends will accrue then we would use the equity equivalent of the expression for a perpetual bond: Duration = 1 / (discount rate – growth rate). We estimate this to be between 30 and 40 years [at present]”

“Equity duration measures the sensitivity of an equity price to changes in the discount rate [here a bond yield plus a risk premium]. By focusing on duration, our assumption is that when QE is scaled back, bond yields will rise. Equity duration depends on three things: the discount rate, the growth rate of dividends and the volatility of dividend growth…long duration stocks are low beta, and have high growth and stable earnings.”

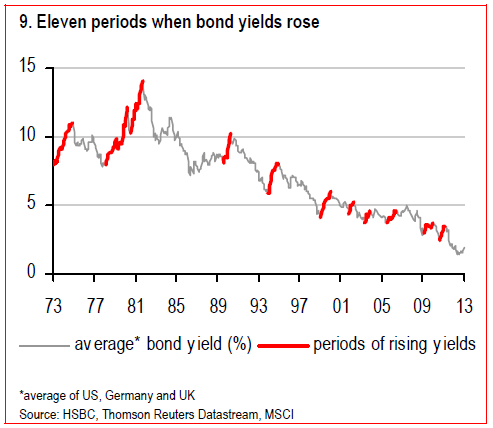

“There have been 11 periods when global bond yields have risen over the past 40 years…They range from five months to a little over two years and saw bond yields rise by 83 basis points to 423 basis points. The longest episode lasted from February 1978 to March 1980 when bond yields rose by over 400 basis points. Some coincide with tightening cycles and some do not…The key message from these episodes is that technology, materials, energy and industrials consistently outperform. These findings are consistent with our duration estimates in that we find these sectors are generally short duration. The weakest performers are consumer staples, utilities and healthcare and we find they are generally long duration.”

“Two of the most persistent trends over the past two decades have been the outperformance of low beta stocks and high quality stocks. The idea that investors can simultaneously increase returns and reduce risk is certainly counter intuitive. Indeed, the strong performance of low beta stocks has been suggested as a candidate for the greatest anomaly in finance…Our work on duration provides quite a different perspective. It suggests there is no anomaly. Low beta is one of the components that contribute to long duration and outperformance is precisely what we would expect when bond yields are falling.”