The cost of insuring against currency volatility can be measured as the difference between (options-based) implied volatility and (swaps-based) forward expected realized volatility. A case can be made that this insurance premium determines how much exposure risk-averse institutions are willing to accept. A new paper and blog post by Della Corte, Ramadorai, and Sarno claim that variations in volatility insurance costs can be the basis for a profitable currency trading strategy.

“Volatility Risk Premia and Exchange Rate Predictability” by Pascuale Della Corte, Tarun Ramadorai, and Lucio Sarno, Working Paper, December 26, 2013

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2233367

http://www.voxeu.org/article/volatility-insurance-and-exchange-rate-predictability

The below are excerpts from the paper and blog. Emphasis and cursive lines have been added.

“Our recent work discovers a new currency strategy with high average excess returns, excellent diversification benefits relative to the set of previously discovered currency strategies. The key to this new strategy is the significant predictive power of the currency volatility risk premium for currency excess returns.”

Understanding the volatility risk premium

“The volatility risk premium [VRP] ,the difference between expected realized and model- free implied volatility, reflects the costs of insuring against currency volatility fluctuations [N.B.: The expected realized volatility is based on the prices for volatility swaps, i.e. forward contracts with a payoff that depends on future realized volatility] …When it is high realized volatility is higher than the option-implied volatility insurance is relatively cheap, and vice versa.”

N.B.: This concept bears similarities and relations to the Variance Risk Premium, which denotes the difference between options-implied and realized volatility. However, the Variance Risk Premium is interpreted as a premium paid for accepting volatility of volatility and, hence, predicts higher returns if the implied volatility is relatively high. View post here.

“In general…literature has shown that the volatility risk premium is on average negative – expected volatility is higher than historical realized volatility, and since volatility is persistent, expected volatility is also generally higher than future realized volatility.”

Explaining the predictive power of volatility risk premia

“Our preferred explanation relies on the presence of limits to arbitrage and its effects on the interaction between hedgers and speculators in the currency market.”

“In the currency markets, this explanation comprises two components. First, it requires time-variation in the amount of arbitrage capital available to natural providers of currency volatility insurance (‘speculators’), such as financial institutions or hedge funds. The second ingredient is risk-averse natural ‘hedgers’ of currencies such as multinational firms, or financial institutions that inherit currency positions from their clients. These hedgers are likely to be more comfortable holding (or entering into contracts denominated in) currencies with relatively inexpensive volatility insurance. Such institutions will also be more likely to avoid positions in currencies with relatively expensive volatility protection. The combination of these two ingredients would be sufficient to generate the patterns that we see in the data.”

“Assume that speculators face a shock to their available arbitrage capital. This limits their ability to provide cheap volatility insurance, especially in currencies in which they have large positions – for example, they may reduce their outstanding short put option positions in the currencies in which they trade…Limits on speculators’ ability to satisfy demand for volatility insurance increase net demand in the options market for the specific currencies in which they are most active, increasing current option prices and making hedging more expensive…Given the high cost of volatility insurance, natural hedgers may scale back the amount of spot currency they are willing to hold, or be more reluctant to get into new expensive hedges. This net demand will predictably depress spot currency rates.”

“The explanation implies that the returns from the VRP strategy, post-formation, should be temporary, i.e., there should be reversion in currency returns once arbitrage capital returns to the market. Confirming this prediction, we find that currency volatility risk-premium sorted portfolio returns reverse over a holding period of a few months.”

“At times when funding liquidity (as measured by the TED spread) is lower, and demand for volatility protection (as measured by VIX) is higher, we find that the spread in the cost of volatility insurance across currencies and the spread in spot exchange rate returns across portfolios both increase…when capital flows to currency and global macro hedge funds are high, signifying increased funding and thus lower hedge fund capital constraints, the returns to VRP are lower and vice versa.”

“Using data provided by the CFTC in their Commitment of Traders reports. We find that commercial traders tend to sell currencies which are more expensive to insure, and buy currencies which are cheaper to insure; in contrast, financial traders appear to trade in a way that is exactly opposite to that of commercial traders.”

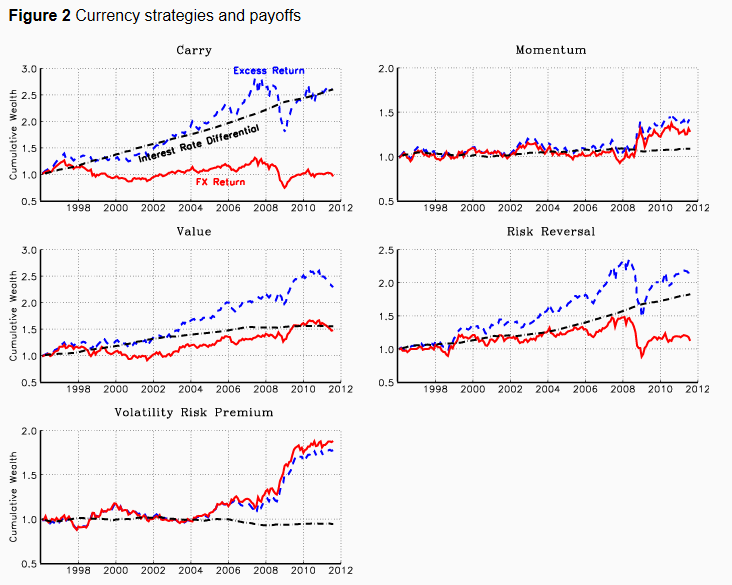

1996-2012 performance characteristic of the VRP strategy

“The strategy is to buy currencies with relatively cheap volatility insurance, i.e., the highest volatility risk premium…The performance of V RP stems virtually entirely from the predictability of spot exchange rates rather than from interest rate differentials. That is, currencies with relatively cheap volatility insurance tend to appreciate over the subsequent month, while those with relatively more expensive volatility insurance tend to depreciate over the next month.”

“A useful summary statistic of the importance of this new currency strategy (which we call VRP), is that over the 1996 to 2011 period, in a cross-section of up to 20 currencies, it has the highest weight (33%) in the global minimum variance portfolio of five well-known currency strategies…The high weight of VRP in the currency strategy portfolio is primarily a reflection of its very desirable correlation properties relative to the other widely studied currency strategies, as VRP does not have the highest returns among the strategies considered. This unusual low correlation partly arises from the excellent performance of VRP during crises, and primarily from the fact that the currency excess returns of VRP are almost completely obtained through predictable variation in exchange rates, rather than from interest rate differentials.”