A new academic paper asserts strong empirical evidence for capital flow deflection: one country’s capital inflow restrictions re-direct capital flows to other countries with similar economic characteristics. While the paper investigates from a policymaker angle, it would be relevant for international macro trading strategies.

“Capital Flow Deflection”, Paolo Giordani, Michele Ruta, Hans Weisfeld, Ling Zhu

http://docenti.luiss.it/giordani/files/2007/09/capitaldeflectionJUNE14.pdf

The below are excerpts from the paper. Cursive text and underscores have been added.

In a nutshell

“In a simple model of capital flows and controls, we show that inflow restrictions distort international capital flows to other countries…We then test the theory using data on inflow restrictions and gross capital inflows for a large sample of developing countries between 1995 and 2009. Our estimation yields strong evidence that capital controls deflect capital flows to other borrowing countries with similar economic characteristics.”

A definition of capital flows and controls

“Gross inflows are the net of foreign purchases of domestic assets and foreign sales of domestic assets. In other words, gross inflows measure the change in the stock of gross foreign liability before any valuation adjustment. Gross outflows measure the change in the stock of foreign assets before any valuation adjustment. Net flows are the difference between the two.”

“Inflow controls…are restrictions imposed on foreign purchases of domestic assets and/or foreign sales of domestic assets….Outflow controls…are restrictions imposed on domestic residents’ purchases of foreign assets or domestic residents’ sales of foreign assets…Both inflow and outflow controls have in common that they discriminate on the basis of residency.”

The narrative behind capital flow deflection

“Governments have two main reasons for influencing capital flows. A first rationale comes from the desire to manipulate the inter-temporal terms- of-trade in their favor [typically in order to make local production more competitive]… The second motive for capital controls is to manipulate the domestic interest rate to address domestic distortions, such as financial fragility [called the prudential motive].”

“Inflow restrictions imposed by a large country, or a sufficiently large set of small countries, lower the world interest rate, as they subtract demand for capital from the world market. This change in the world interest rate leads to higher borrowing by recipient countries that have not altered their capital controls.”

“The cross-border policy spillover effect among borrowers is what we refer to as capital flow deflection… As international investors perceive a lower return of exporting capital to countries that tightened capital controls, they reallocate their capital to the other borrowers.”

“If the primary motive for capital controls is to manipulate the domestic interest rate, as for prudential controls, then uncoordinated inflow restrictions can magnify exogenous shocks… Intuitively, with capital flow deflection, inflow restrictions are complementary policies, so that a shock initiates a chain reaction and leads to a multiplier effect.”

The empirical evidence

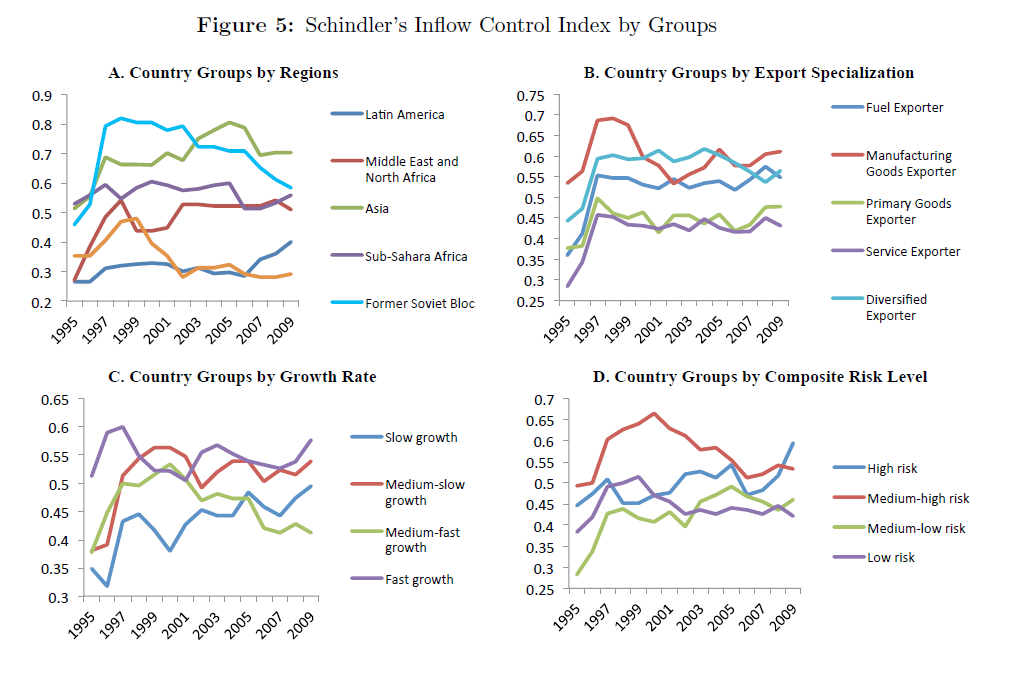

“In the empirical investigation, we use a dynamic panel model to estimate the impact of capital controls on inflows to other countries and on the policy response…We use data on gross capital inflows for a large sample of [78] developing countries between 1995 and 2009… We use Schindler’s (2009) index of capital controls, which is a de-jure measure constructed from information contained in the Annual Report on Exchange Arrangements and Exchange Restrictions provided by the IMF…Schindler’s index calculates inflow controls as the average of the restriction dummies on…international transactions.”

“We find strong evidence of a capital flow deflection. The spillover effect of inflow restrictions is estimated to be strong and significant among borrowing countries that have similar risk level. Perhaps surprisingly, we find no significant spillover effects on countries in the same region. This finding is consistent with the view that investors are guided by similar economic characteristics of countries, rather than their geographic location -a result that confirms in a cross-section the evidence of existing event studies.”

“Capital flow deflection is also found to be economically relevant. While somehow an extreme case, we estimate that gross inflows to South Africa as a share of GDP would have been between 0.5 and 1.0 percent lower if Brazil had not imposed higher inflow restrictions in 2009.”

“Notwithstanding the strength of capital flow deflection, we find no evidence of a policy response [of the recipient countries of deflected flows]. This result is independent of how we group countries and persists even if we focus on small economies, which have no terms-of-trade motives to set capital controls.”