Macroprudential measures are often seen as a counterweight to ultra-easy monetary policy in the developed world. BIS research cautions against this expectation. Macroprudential policies are largely new and untested, have worked best as a complement (not offset) to monetary policy, and focus on specific sectors, such as banking and housing.

The below are excerpts from the various papers and speeches, as listed at the end of the post. Headings and cursive text have been added.

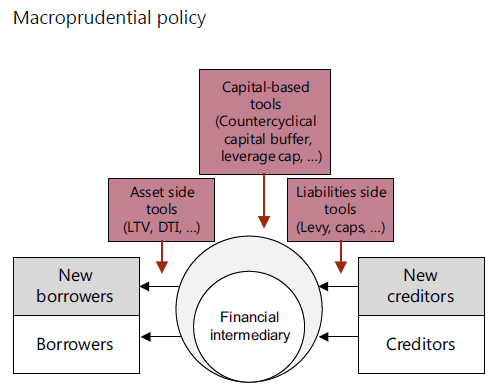

Macroprudential policy is a countercyclical policy

“A key aim of macroprudential policy is to moderate the pro-cyclicality of the financial system and it does so by influencing the financial intermediation process; it operates on the assets, liabilities and leverage of intermediaries [graph below]. In this respect, macroprudential policy and monetary policy share some similarities.” [Shin 2015]

“Macroprudential policy… is the regulation and supervision of the financial system as a whole rather than just the ‘micro’ regulation and supervision of the firms and the markets that go to make up the system…the basic principles of macroprudential policy are:

- the financial system…feeds on its own exuberance in good times and on its fear in bad times which can in turn drive the real economy to extremes…the aim of macroprudential authorities should be to prevent these dynamics from driving up financial stability risks in good times and driving the system down in bad times…

- the objective of ensuring the financial system as a whole is stable is different to the objective of promoting the safety and soundness of individual firms or that inflation is kept at target…the stability of individual financial firms will not… assure the stability of the overall financial system…

- the reserves of capital and liquid assets that individual banks and other firms need to hold…should be set not simply in relation to the risks in the individual firm, but also to reflect the importance of the firm to the financial system.” [Cunliffe, 2015]

“There are at least two inter-related reasons for using macroprudential policies: (i) to create a buffer (or safety net) so that banks do not suffer overly heavy losses during downturns; and (ii) to restrict the build-up of financial imbalances and thereby reduce the risk of a large correction.” [McDonald 2015]

Macroprudential policy is not a separate from monetary policy

“The separation principle has the merit of yielding clear and neat policy assignments: monetary policy for price stability and macroprudential policy for financial stability….This principle is…not very convincing…for three reasons.

- Both macroprudential policy and monetary policy fundamentally influence the same channels – funding costs, leverage incentives and risk-taking…As such, these two policies are not really neatly separable…The two sets of tools are most effective when used as complements, pulling in the same direction… even using both macroprudential and monetary policies may still be insufficient in some situations because the endogenous build-up of financial imbalances can be very powerful.

- Experience suggests that…macroprudential policy tools…are not as effective as monetary policy rates in preventing excessive risk-taking that is widespread across the financial system…They cannot ‘get in all the cracks’ in the system…Arbitrage can move the build-up of financial imbalances from one place to another, finding the inevitable cracks that exist in any prudential regulatory regime.

- Most of our experience so far with macroprudential tools has come from banking. But now, imbalances are building not so much in the banking sector but in capital markets, which are not within the direct reach of traditional macroprudential tools.” [Caruana, 2015]

“Much recent discussion of macroprudential policies in advanced economies treat the two sets of policies as being substitutes that is, monetary policy is kept loose but macroprudential policies are invoked to deal with the financial stability implications of such loose policy….We conduct a comparative empirical assessment of the impact of broadly-defined macroprudential measures taken in 12 Asia-Pacific economies over 20042013…Detailed examination of our databases reveals that the most effective instances of the use of macroprudential policies are when they complement monetary policy, by reinforcing monetary tightening rather than acting in the opposite direction…Such a conclusion is also consistent with the principle that when monetary policy and macroprudential policies pull in the opposite direction, economic agents are being told simultaneously to borrow more and borrow less.” [Bruno, Shim and Shin, 2015]

Macroprudential policy is largely untested

“[We] put too much faith in the ability of macroprudential policy to deal with financial stability risks but underappreciate monetary policy’s role in determining the price of leverage and in influencing borrowing and risk-taking behaviour across the board…Exclusive reliance on macroprudential tools to deal with financial stability risks is insufficient and ill advised…Current models and traditional analytical approaches take little or no account of the endogenous cumulative effects of interest rates being too low for too long. They tend to assume that monetary policy has limited influence on the financial cycle – and hence on the costs of financial booms and busts. The international dimension of monetary policy, the spillovers and spillbacks, also tend to be underestimated.” [Caruana, 2015]

“There are now macroprudential authorities in around 40 jurisdictions. But there are very different views among policymakers as to what time-varying, countercyclical macroprudential should and could do….There is still a great variety of views as to how macroprudential policy should identify and respond to changing risks in the financial system. There is no consensus about which risks it should care about and which instruments are most effective in addressing them. There is not yet the extensive body of practice and of theoretical and empirical research that exists, for example, in the world of monetary policy.” [Cunliffe, 2015]

Macroprudential policy is usually aimed at specific sectors

“Most of the experience with macroprudential tools to date has come from banking. There is relatively little knowledge as to what policy measures could be taken to address the build-up of financial excesses that originate from outside the banking system… A relevant consideration here is the way in which credit intermediation is moving away from the banking sector to the debt securities market.” [Caruana 2014]

“Loan-to-value (LTV) and debt-to-income (DTI) limits have become increasingly popular tools for responding to house price volatility…[reflecting evidence of] the effectiveness of macroprudential policies at taming real estate cycles…By looking at 100 policy adjustments across 17 economies, I find that changes to LTV and DTI limits tend to have bigger effects when credit is expanding quickly and when house prices are relatively expensive… Tightening LTV and DTI limits appears to be more effective than loosening them…Tightening measures (such as lowering the maximum LTV ratio) during upturns lower the level of housing credit over the following year by 4-8 percent and the level of house prices by 6-12 percent. Conversely, during downturns they reduce housing credit by 2-3 percent and house prices by 2-4 percent.” [McDonald 2015]

Sources

Bruno, Valentina, Ilhyock Shim and Hyun Song Shin (2015), “Comparative assessment of macroprudential policies”, BIS Working Papers No 502, June 2015 http://www.bis.org/publ/work502.pdf

Caruana, Jaime (2015), “Revisiting monetary policy frameworks in the light of macroprudential policy”, panel remarks at the IMF seminar on “Revisiting monetary policy frameworks” Lima, 10 October 2015 http://www.bis.org/speeches/sp151130.htm?ql=1

Caruana, Jaime (2014), “Macroprudential policy: opportunities and challenges”, Speech in Abu Dhabi, United Arab Emirates, 9 December 2014 http://www.bis.org/speeches/sp141219.pdf

Cunliffe, Jon (2015), “Macroprudential policy: from Tiberius to Crockett and beyond”, Speech at TheCityUK, London28 July 2015 http://www.bankofengland.co.uk/publications/Pages/speeches/2015/836.aspx

McDonald, Chris (2015), “When is macroprudential policy effective?”, BIS Working Papers No 496, March 2015 http://www.bis.org/speeches/sp150415.pdf

Shin, Hyun Song (2015), “Macroprudential tools, their limits and their connection with monetary policy”, panel remarks at IMF Spring Meeting event: “Rethinking macro policy III: progress or confusion?” 15 April 2015, Washington, DC http://www.bis.org/speeches/sp150415.pdf