Another (IMF) paper of Manmohan Singh deals with the influence of non-conventional monetary policy on collateralized borrowing. In past years, quantitative easing (QE) has absorbed collateral from private funding markets and, thereby, reduced private repurchase (collateral) rates relative to policy rates. An unwinding of central bank balance sheets in the future could increase the spread between policy and collateral rates – if the collateral finds its way on bank balance sheets – or reduce the degree of financial “lubrication” – if it ends up with non-banks. Put differently, in a large-scale QE unwind central banks could temporarily lose control over lending conditions.

“Collateral and Monetary Policy”, Manmohan Singh

IMF Working paper WP/13/186, August 2013

http://www.imf.org/external/pubs/ft/wp/2013/wp13186.pdf

The below are excerpts from the paper. Cursive text and emphasis have been added.

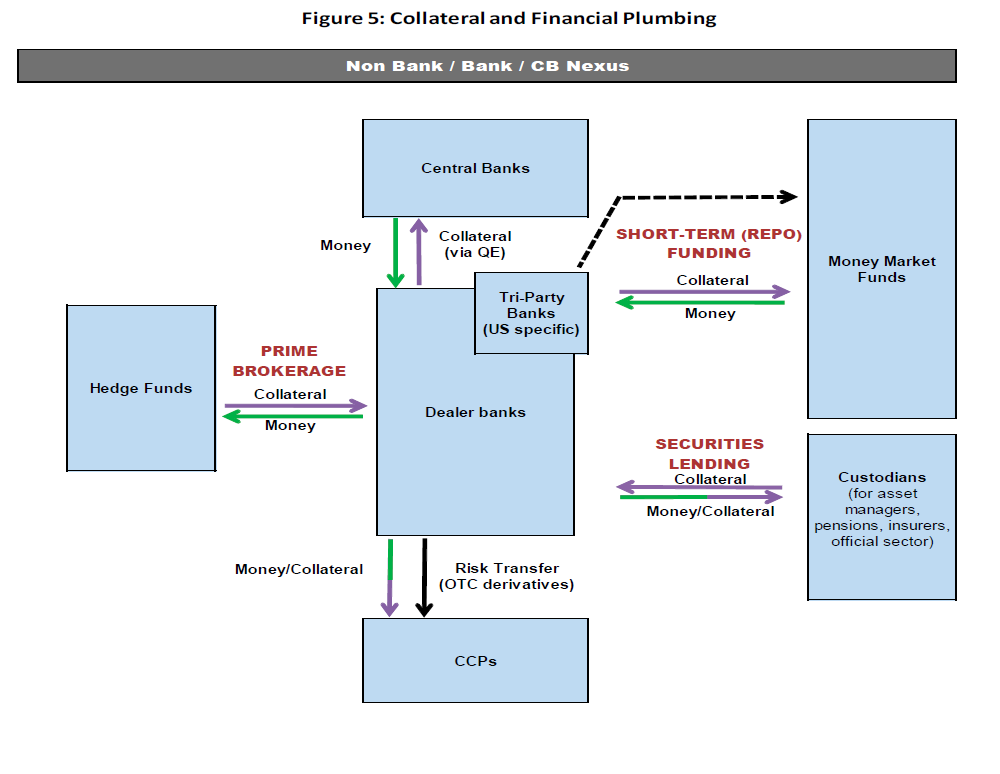

Reiterating the point of collateral and financial intermediation

A framework of thinking about collateral and QE

“Although there is a continuum between good and bad collateral, for simplicity we define C1 that is good collateral in all states of nature and can be converted to money or deposits including excess reserves (D) at no haircut. C2 is collateral that under normal market conditions is “good” but otherwise loses value. During a crisis, C1 (such as U.S. Treasuries or Bunds) and D may continue to be acceptable at par. There is a sudden split between D+C1, and everything else.”

“To the extent that central banks merely substitute central bank money (D) for assets that have retained their value as collateral (C1), not much liquidity relief is achieved. In order to provide effective liquidity relief for the system, central bank money and liquid collateral must be injected against illiquid or undesirable assets (C2); the supply of unencumbered collateral has to increase. Central banks became subject to a form of Gresham’s Law (i.e. “bad collateral will drive out good collateral from markets”) if they were slow or reluctant to loosen their collateral policies.”

“The past few years since Lehman has seen major central banks take out good collateral from markets and replace it with freshly printed money (except the ECB which has printed money but taken in bad collateral). Sooner or later, these balance sheets will unwind—either voluntarily when central banks will release collateral and take in money, or involuntarily as the securities held at central banks mature or roll-off.”

The consequences of unwinding QE

“Sooner or later [central bank] balance sheets will unwind…unwind will increase both, the (money) interest rate and the (collateral) repo rate…Analogous to a coiled spring, the larger the QE efforts the lesser the control central banks may have on the “wedge” between repo rates and their policy rate. This is likely to result in very little collateral release to the markets [in the first place]…Central banks that have withdrawn collateral via QE will be the biggest holder of good collateral.”

“When central banks buy securities, one of the immediate effects is to increase bank deposits, which adds to M2 (in the U.S., practically the Fed has bought from nonbanks, not banks)… At present, the Fed has proposed a reverse repo program to unwind its balance sheet; however this will be contingent on balance sheet “space” at banks and nonbanks amidst a tighter regulatory environment (and the interaction of repo and policy rates). With Basel III regulations at the door, the banking system is likely to have limited appetite for these securities except for capital buffers. Nonbanks “balance sheet space” is key to any unwind of collateral.”

“However, the excess reserves are on bank balance sheets now…collateral with these nonbanks via reverse repos cannot be rehypothecated, or onward re-pledged, and thus will not contribute towards financial lubrication. So collateral released to nonbanks will not convert D [excess reserves] to C1 [good collateral]; But…collateral release to nonbanks will avoid any jumps in repo rates (as this is a necessary condition when policy rates lift off).”