Simple regression is inadequate for predicting bond returns, as the character of rates markets changes fundamentally with economic conditions. In financial modelling terms this calls for time-varying parameters, time-varying volatility, and model uncertainty. A CEPR paper claims that these features can help turning standard forecast factors (forward rates, forward spreads, and macro) into a valuable prediction model.

Gargano, Antonio, Davide Pettenuzzo, and Allan Timmermann (2014), “Bond Return Predictability: Economic Value and Links to the Macroeconomy”, CEPR Discussion Paper 10104, August 2014

http://www.cepr.org/active/publications/discussion_papers/dp.php?dpno=10104

or http://rady.ucsd.edu/docs/faculty/timmerman/bond-return-predictability.pdf

The below are excerpts from the paper. Emphasis and cursive text have been added.

What it takes to build a bond return forecast model

“Modeling bond return dynamics requires adding several features that are absent from the regression models used in the existing literature.

- First, bond prices, and thus bond returns, are sensitive to monetary policy and inflation prospects, both of which are known to shift over time. This suggests that it is important to adopt a framework that accounts for time varying parameters and even for the possibility that the forecasting model may shift over time, requiring that we allow for model uncertainty… we address model uncertainty through model combination methods.

- Second, uncertainty about inflation prospects changes over time and the volatility of bond yields has also undergone shifts, most notably during the Fed’s monetarist experiment from 1979-1982– underscoring the need to allow for time-varying volatility… we find clear advantages from allowing for stochastic volatility beyond this episode…

- Third, risk-averse bond investors are concerned not only with the most likely outcomes but also with the degree of uncertainty surrounding future bond returns, indicating the need to model the full probability distribution of bond returns…

An ensemble of such extensions to the constant mean, constant volatility model is required to establish evidence of significant out-of-sample return predictability.”

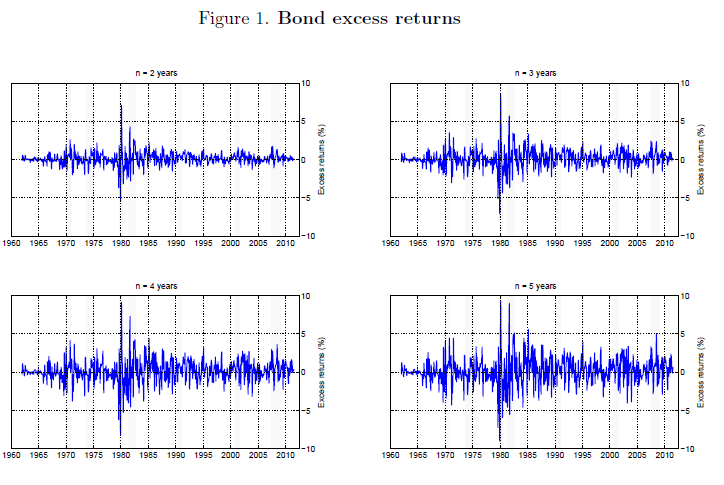

N.B.: The above charts show monthly government bond excess returns for maturities of 2-5 years and illustrates the significant differences in variance over time.

A suggested forecast model

“Our empirical strategy entails regressing bond excess returns on a range of the most prominent predictors proposed in the literature on bond return predictability. Specifically, we consider forward spreads as proposed by Fama and Bliss (1987), a linear combination of forward rates as proposed by Cochrane and Piazzesi (2005), and a linear combination of macro factors, as proposed by Ludvigson and Ng (2009)… the Fama-Bliss spreads…are positive correlated with the…[forward rates] factor, with correlations around 0.5, but are uncorrelated with the…[macro] factor. The… [macro] factor captures a largely orthogonal component in relation to the other predictors…

Each variable is weighted according to its ability to improve on the predictive power of the bond return equation… Since forecasting studies have found that simpler models often do well in out-of-sample experiments, we also consider simpler univariate and bivariate models that include one or two predictors.”

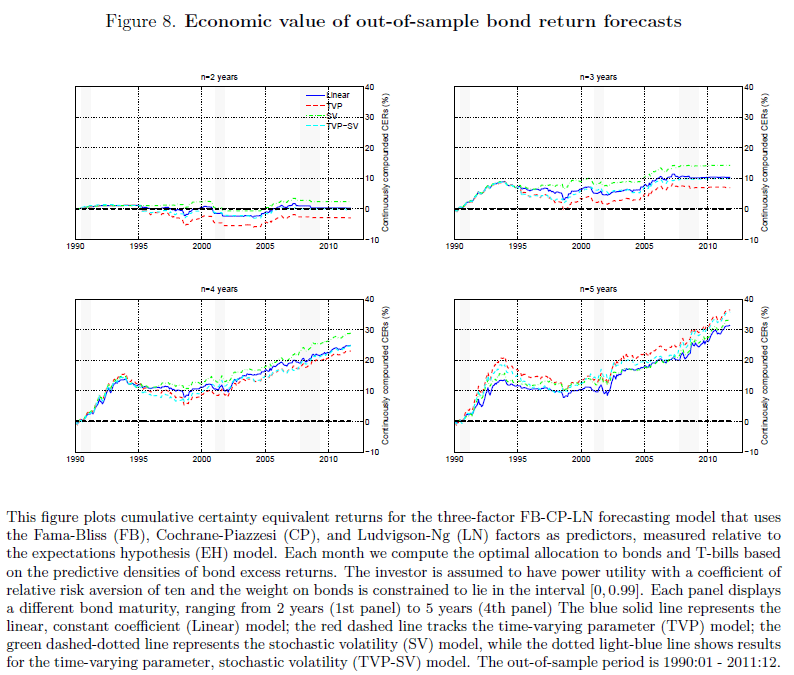

“Allowing for stochastic volatility and time varying parameters, while accounting for parameter estimation error, leads to important gains in economic performance for many models…Such gains in predictive accuracy translate into higher risk-adjusted portfolio returns after accounting for estimation error and model uncertainty, as evidenced by the performance of model combinations. “

Empirical findings

“Our empirical analysis uses the daily treasury yield data…to construct monthly excess returns for bond maturities between two and five years over the period 1962-2011… To assess the statistical evidence on bond return predictability, we use our models to generate out-of-sample forecasts over the period 1990-2011. Our return forecasts are based on recursively updated parameter estimates and use only historically available information, thus allowing us to assess how valuable the model forecasts would have been to investors in real time.”

“We find that the best return prediction models that account for volatility dynamics and changing parameters deliver sizeable gains in certainty equivalent returns relative to a… model that assumes no predictability of bond returns…We conclude…that there is strong statistical and economic evidence that the returns on 2-5 year bonds can be predicted using predictor variables proposed in the literature. Moreover, the best performing models do not assume constant parameters but allow for a time varying mean and volatility dynamics.”

“Comparing results across predictor variables, the [forward rates] model is never found to improve the predictive accuracy…Moreover, there is only modest evidence that the [forward rates] variable, when added to any of the other predictors, results in improved performance. Conversely, the [forward spreads] and [macro] two-factor model performs best across the four maturities.”

“We find strong evidence that bond return predictability is stronger in recessions than during expansions, consistent with similar findings for stock returns… Economic theory suggests that treasury bond risk premia should be driven by time-varying inflation uncertainty as well as variations in the market price of this source of risk. Using data from survey expectations we find that our bond excess return forecasts are strongly negatively correlated with economic growth prospects (thus being higher during recessions) and strongly positively correlated with inflation uncertainty. This suggests that our bond return forecasts are, at least in part, driven by time-varying risk premia.”