Asset managers can use leverage to enhance returns. Outside hedge funds, such leverage is modest as share of assets under management. However, considering the huge volume of assets, changes in buy-side leverage still have a significant impact on financial conditions, particularly in emerging markets. Also, both theory and empirical evidence suggest that leverage is pro-cyclical.

Avalos. Fernando, Ramon Moreno and Tania Romero, “Leverage on the buy side”, BIS Working Papers, No 517

http://www.bis.org/publ/work517.htm

The below are excerpts from the paper. Headings, links and cursive text have been added.

The 1×1 of leverage on the buy side

“Leverage used by an investment fund can [use]…funding leverage, which involves outright borrowing, and instrument leverage [also called synthetic leverage], implemented through derivative contracts that amplify the sensitivity of portfolio returns to the underlying asset risk factors.”

On the rising trend in synthetic leverage among euro area asset managers and related stability issues view post here.

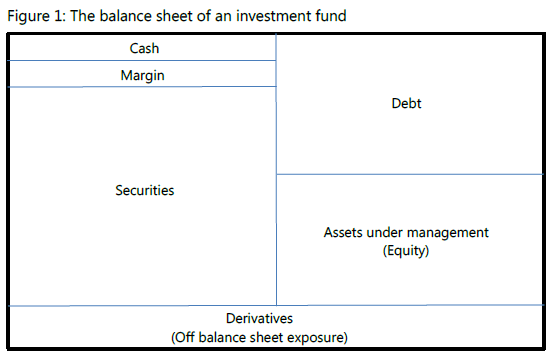

“[The figure below] represents the typical balance sheet of a fund. On the source side we have its capital structure, comprising debt and the assets under management (AUM). Debt corresponds to short cash positions (or short-term borrowing) and short security positions. AUM is the difference between the fund´s asset and liability positions, and represent the total claim individual investors have on the investing pool. On the asset side we have cash held in long positions, securities held in long positions and margin, i.e. collateral typically requested by lenders in order to extend credit. Derivatives can be assets or liabilities depending on whether they are held long or short, but they are in effect off-balance sheet contingent claims. The relative size of all these different parts will depend on the type of fund and portfolio strategy. For instance, hedge funds are likely to have the largest borrowing relative to AUM, whereas passive mutual funds aimed at retail investors are likely to have minimal debt and relatively small long cash positions. Distressed debt funds use little or no leverage and keep a large share of their portfolio in cash.”

“Leverage is usually defined as…gross leverage, net leverage and long leverage. Gross leverage adds the short and long positions in securities, divided by AUM. This measure is very conservative, since it treats the short and long positions as independent sources of revenue, while in many cases they are part of a single bet and tend to hedge each other. As a result, gross leverage tends to overstate economic exposure. Net leverage is the difference between long and short positions in risky assets, which corrects the bias of gross leverage but does not account for the risk created by long or short positions that are effectively independent bets. Thus this measure is likely to understate risk. Finally, long leverage is the ratio of long security positions to AUM. This is probably the easiest and more common way to think about leverage. It is readily available for US-based institutions, because the SEC requires this information from any fund managing over USD 100 million. All the above measures of leverage also ignore the exposure from off-balance sheet derivative positions.”

“Leveraged portfolios enhance the gains of successful investment strategies, at the cost of magnifying the losses when financial conditions sour. Consequently they may be subject to severe allocation reversals and fire sales, which could sharpen the return volatility of the assets included in such portfolios.”

Different funds have different leverage

“Since [the great financial crisis]…asset managers have quickly increased their footprint in global financing, helped by the sharp retrenchment of banks nursing their balance sheets back to health…Since 2009, bond financing has become prevalent in global international financing, with an expansion exceeding USD4 trillion, whereas cross border bank lending has contracted by almost USD2 trillion…Unconventional monetary policies in advanced economies have squeezed returns while reducing borrowing costs, which in principle creates an incentive for asset managers to use more leverage.”

“Using information provided by a market data vendor…[leverage] seems to vary considerably depending on the type of fund… In most of the analysis…we focus on funding leverage by using a measure closely related to long leverage… the ratio of long security positions in excess of AUM divided by AUM….Equity fund portfolios seem to be minimally leveraged, while fixed income funds tend to resort abundantly to borrowed money. Funds dedicated to global markets or advanced economies had little debt in their capital structure, whereas debt in leveraged EM fixed income funds was close to 30 percent of AUM towards the end of our sample period.“

“We found that leverage on the buy side is not negligible [for emerging markets]. The number of funds using leverage is relatively small in our sample, but their size is about three times that of their unleveraged peers. They control more than 30 percent of AUM in their sector [at the end of 2014] down from 50 percent around 2010, making them quite significant players in their target markets…Only four of the 87 funds in our database report themselves as ‘hedge funds,’ all belonging to the same parent company.”

Determinants of leverage on the buy side

“In line with theory, we find that asset managers increase leverage when expected returns increase, and tend to reduce it when market risk perception (or aversion) increases, or when funding costs or funding risks increase. Leverage is also pro-cyclical, in the sense that fund capital gains spur further increases of borrowing.”

This is consistent with other evidence on the pro-cyclicality of EM bond funds as summarized in another post here.

Other academic work supports this pro-cyclicality:

- “Acharya and Viswanathan (2011) and Stein (2009) focus on borrowing costs as the main drivers of leverage, finding through different mechanisms that good times tend to increase leverage substantially. Price shocks during those times are particularly damaging because they force a larger extent of deleveraging.”

- “Ang et al (2011) use a richer database than ours to address empirically a similar question on the determinants of the leverage decision of asset managers… They find that…past returns are not significant, whereas market risk at either the fund or macro levels can be relevant, and macro measures of borrowing costs are usually inversely related to leverage.”

- “Wang and Wang (2010) model the problem of the fee-maximising, risk-neutral investment manager…Consistent with some anecdotal evidence, asset managers have little incentive to sell assets and reduce leverage unless forced to, once the risky asset price has fallen. However, optimal leverage tends to decrease quickly with higher transaction costs and underlying asset price volatility, whereas it will increase with expected returns.”

“The tightening of capital controls on inflows in emerging economies seems to be associated with leverage increases, which might be explained by reluctance on the part of portfolio managers to give up a profitable position because of returns-unfriendly regulation. Instead, they would choose to increase leverage in order to preserve higher expected returns, even at the cost of assuming more risk… In this way, ‘capital flow management’ actions taken by large emerging economies, which tend to command large portfolio weights, might be causing a ‘policy spillover’ towards other emerging economies that are commonly represented in the portfolios of global asset managers.”

For more on capital controls and ‘capital flows deflection’ view post here.