A new Review of Finance article investigates the link between commodity inventories on the one hand and futures returns and curve backwardation on the other. Most prominently, low inventories mean that the convenience yield of physical holdings is high (more need of insurance against a “stock-out”). In this case, producers and inventory owners are willing to pay a surcharge for immediate access to the physical. This will (normally) translate into a higher risk premium, more backwardation, and higher expected excess returns. Moreover, external factors, such as price volatility, can induce producers and physical inventory holders to pay a higher premium for future price certainty that translates into a positive basis and expected return on futures positions. The inventory connection explains why commodity futures returns and futures curve shape are correlated, i.e. backwardation is more often than not a profit opportunity. According to this paper, mainstream theory is backed by empirical evidence for 31 commodities over more than 40 years.

The Fundamentals of Commodity Futures Returns

Gary B. Gorton, Fumio Hayashi and K. Geert Rouwenhorst

Review of Finance, 2013, vol. 17, issue 1, pages 35-105

http://rof.oxfordjournals.org/content/17/1/35

The basic theory

Established theories of commodity futures suggest that the inventory level of a physical commodity is a fundamental driver of its risk premium and basis. Other factors, such as price volatility, may affect both inventory and risk premiums paid to financial investors:

N.B. According to the Theory of Storage, in equilibrium the basis of a storable commodity is equal to convenience yield minus both funding costs and storage costs.

“There is a modern, optimization-based version of the Theory of Storage that emanates from Deaton and Laroque (1992). Inventories act as buffer stocks which help to absorb shocks to demand and supply affecting spot prices. But inventories cannot be negative (goods cannot be transferred from the future to the past), so there is a possibility of a stock-out in which non-negativity constraint on inventories binds [implying that the basis can surge in times of shortage). Routledge, Seppi, and Spatt (2000)…show how the convenience yield arises endogenously as a function of the level of inventories and supply and demand shocks. Even if there is no direct benefit from owning physical inventories, the convenience yield can be positive because inventories have an option value due to a positive probability of a stock-out.”

“The Theory of Normal Backwardation of Keynes (1930) and Hicks (1939) assumes that commodity producers and inventory holders hedge future spot price risk by taking short positions in the futures market. To induce risk-averse speculators into taking the opposite long positions, current futures prices are set at a discount (i.e., is “backwardated”) to expected future spot prices at maturity. The commodity futures risk premium is the size of this discount.”

“Modern formulations of the Theory of Normal Backwardation (Stoll 1979 and Hirshleifer 1988, 1990) make two basic assumptions. First, the revenue from the physical control of a commodity by hedgers is non-marketable. This assumption might be justified if hedgers in the futures markets are either privately held firms or individual farmers. Second, participation in commodity futures markets by outside investors is limited by some (possibly informational) entry barriers, so a positive risk premium will not be competed away. [Hence], the commodity futures risk premium consists of not only the systematic risk (i.e., the covariance with the market portfolio of traded assets) but also a component related to the volatility of spot prices.”

Empirical analysis and findings

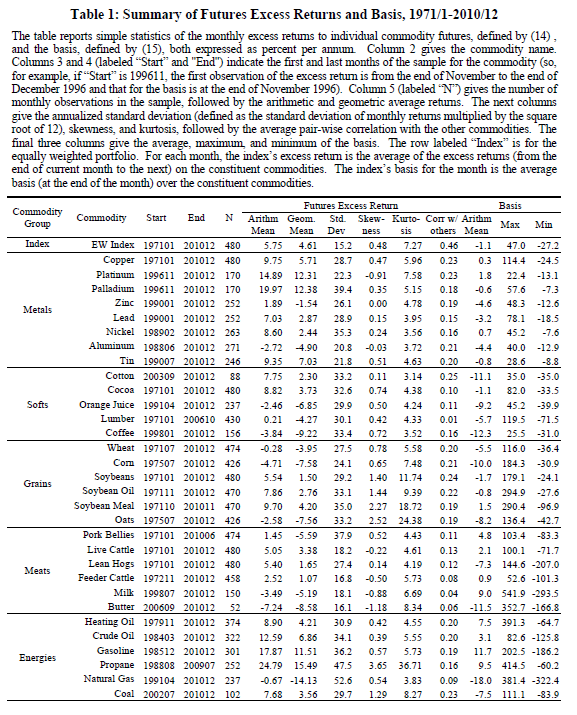

“The main contribution of our paper is an empirical examination of the effect of inventories on the basis and the risk premium articulated by the theory just outlined… by using a comprehensive dataset on 31 commodity futures and physical inventories between 1971 and 2010…We collect a comprehensive historical dataset of inventories for 31 individual commodities over a 40-year period between 1971 and 2010.”

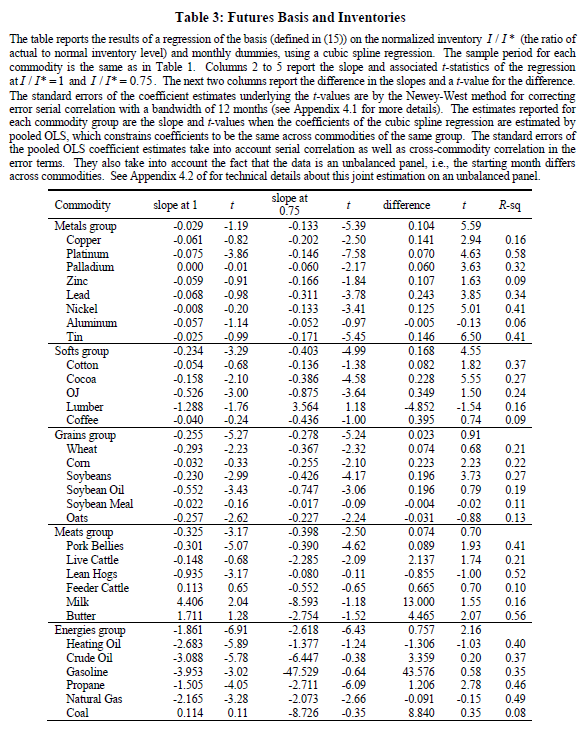

1. The basis tends to increase as inventories decline

“We find that there is a clear negative relationship between normalized inventories [inventories divided by their normal levels] and the basis and that for many commodities the slope of the basis-inventory curve becomes more negative at lower inventories levels. And we find steeper slopes at normal inventory levels for commodities that are difficult to store….When inventories are in a normal range (no stock-out), the estimated slope of the basis-inventory regression is negative for all commodities except four, and statistically significant at 5% for about a half of the commodities…

Cross-sectional differences in storability are reflected in the sensitivity of the basis to inventories. The relationship is particularly strong for Energies (bulky and more difficult to store), while many Industrial Metals (easy to store) tend to have slope coefficients that are relatively small in magnitude…. Industrial Metals are relatively easy to store, and the normal inventory level I* would be large relative to demand… Storability also helps to explain why the slope coefficients for Meats are on average smaller in magnitude than for commodities in the Softs and Grains groups.”

2. Also the risk premium declines with inventory.

“We perform a linear regression of the monthly excess return on the normalized inventory level I / I * at the end of the prior month as well as monthly dummies…As is apparent from the low t-values, the normalized inventory coefficients are not sharply estimated. However, most of them have the expected negative sign. If we impose the restriction of a common slope coefficient within groups, we find significant negative and quantitatively large slope coefficients for all commodities except for the easy-to-store Metals.”

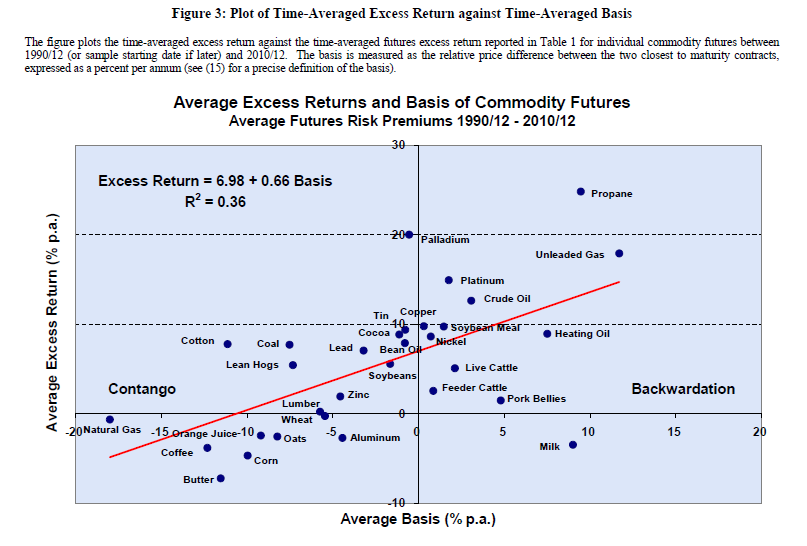

3. The basis is correlated with future excess returns

“The level of inventories is a noisy measure of the true state of inventories because of demand shocks. Also, there is a conceptual question about the relevant inventory measure. These considerations motivate us to examine other signals of the current state of inventories. [In particular] low-inventory commodities [should be associated with] a higher basis, higher prior excess and spot returns…

We show that prior futures returns, prior spot price changes and the futures basis are correlated with futures risk premiums as predicted by the Theory… Portfolios that take positions based on the futures basis, prior futures excess returns, prior spot returns, or volatility select commodity futures with below normal inventories which our theory predicts are expected to earn higher risk premiums. Moreover, these risk premiums are highly significant, both in a statistical sense as well as in an economic sense.”

N.B.:” There are many issues involved in compiling a dataset on inventories… Because most commodity futures contracts call for physical delivery at a particular location, futures prices should reflect the perceived relative scarcity of the amount of the commodity which is available for immediate and future delivery at that location. For example, data on warehouse stocks of industrial metals held at the exchange are available from the LME, but no data are available on stocks that are held off-exchange but that could be economically delivered at the warehouse on short notice. Similarly, relevant Crude Oil inventories would include not only physical stocks held at the delivery point in Cushing, Oklahoma, but also oil which is held at international locations but that could be economically shipped there, or perhaps even government stocks.”