The IMF, like other institutions, estimates that China’s fiscal position is much weaker than suggested by headline statistics. A new paper sees the augmented fiscal debt at around to 45% of GDP and the augmented fiscal deficit at close to 10% of GDP. Financial stability risks arise from dependence on a favorable ratio of growth to real interest rates, the reliance of local budgets on real estate sales, and the refinancing of local government financing vehicles’ debt.

“Fiscal Vulnerabilities and Risks from Local Government Finance in China”, Yuanyan Sophia Zhang ; Steven Barnett

IMF Working Paper No. 14/4

http://www.imf.org/external/pubs/ft/wp/2014/wp1404.pdf

The below are excerpts from the papers. Cursive text and emphasis has been added.

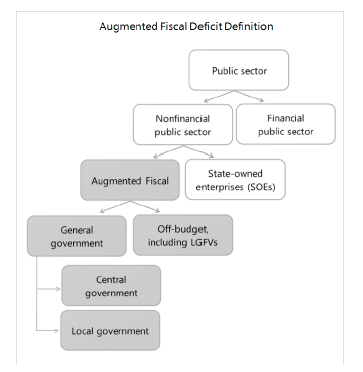

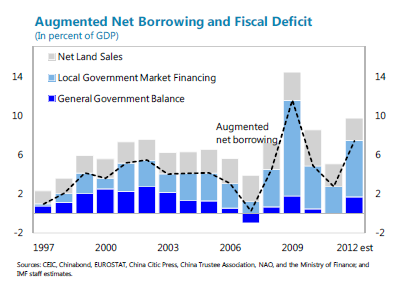

Augmented fiscal data in China

“Infrastructure investment has become local governments’ main strategy to foster growth… Local governments, meanwhile, are for the most part prohibited from borrowing, at least through the budget…Local infrastructure spending has mainly been financed off-budget, either through land sales or Local Government Financing Vehicle (LGFV) borrowings… In simple terms, the local government would create a company that would then borrow from banks, trust companies, or the bond market.”

“Therefore, IMF staff have developed a new ‘augmented’ concept in an attempt to capture these off-budget fiscal activities, which expands the perimeter of the government to include off-budget and LGFV activity. LGFV are different from other state-owned enterprise (SOEs) as LGFVs are largely set up, owned, and operated by the local governments; they engage in economic activities that are fiscal in nature; and the government directly or indirectly shares the debt servicing responsibilities, and sometimes subsidizes their losses.”

“Some quasi-fiscal activity is excluded, such as that carried out by state owned enterprises and policy banks (which are still virtually all state owned). At the same time, by focusing on deficits and debt, the “augmented” fiscal data also ignores the substantial net worth of state owned enterprises as well as their operating profits.”

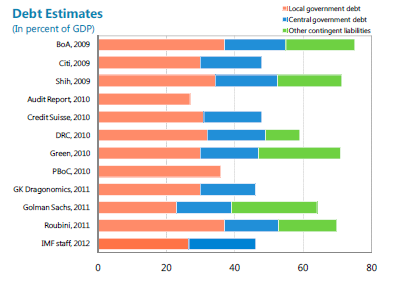

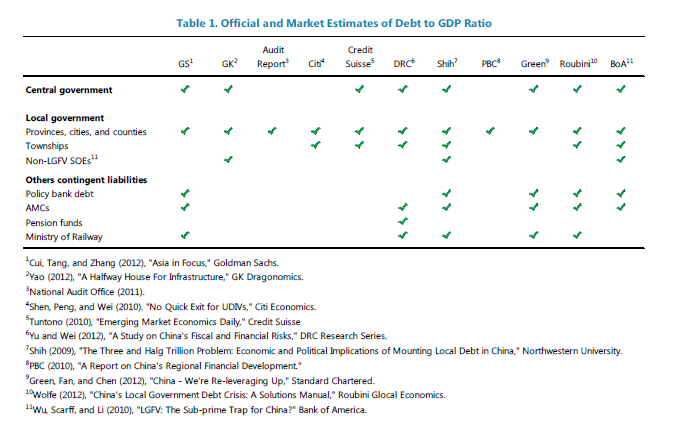

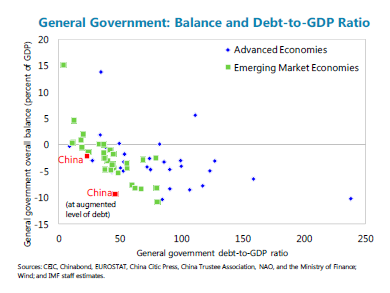

The size of China’s augmented fiscal debt

“Our estimate, of around 45 percent of GDP in 2012, is broadly in line with other estimates after adjusting for these differences. Focusing just on the overall figure, estimates tend to vary from just below 30 percent to above 70 percent of GDP… some include contingent liabilities (such as financial sector liabilities related to asset management companies or development banks) and debt of the Ministry of Railways, which was corporatized in 2013.”

The size of China’s augmented fiscal deficit

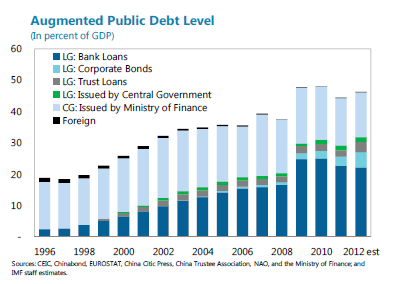

“We introduce two concepts of the augmented fiscal balance. Augmented net borrowing…corresponds to the financing needs of the augmented government, and thus closely matches changes in the augmented fiscal debt. [Augmented net borrowing is estimated at close to 7% of GDP for 2012.]”

“The second concept is the augmented fiscal deficit. This treats the net proceeds from land sales as a financing item, and thus makes the augmented fiscal deficit larger than the change in augmented net lending. [The augmented fiscal deficits has been estimated at close to 10% of GDP for 2012.]”

“Fiscal policy has been considerably more countercyclical than suggested by the general government data. From 2007 to 2009, the augmented fiscal deficit increased by around 10 percent of GDP. This helps explain why, despite the significant global headwinds, China was still able to grow by around 9 percent in 2009. Augmented fiscal policy…The augmented fiscal deficit was unwound rapidly and by 2011 had been reduced by around 8 percent of GDP from its peak. In 2012, in response to sluggish activity in the first part of the year, the augmented fiscal deficit increased by around 4 percent of GDP relative to 2011.”

The importance of land sales

“China’s recourse to land sales is not unusual. Land is often a local government’s most valuable assets, making land sales a natural way to support urbanization. For example, Cairo, Istanbul, and Mumbai have raised significant revenue from land auctions. Some advanced economies such as the United States, Japan, and Korea also went through a similar process during their transition period.”

“Lands sales are a major source of risk for local government finances. First, local government’s reliance on land sales for financing could result in an over-supply of real estate that, in turn, may result in a market correction. A correction, moreover, could trigger a negative feedback loop. Local governments would have to cut spending as proceeds from land sales fell, at the same time that a decline in construction activity would already be hurting local fiscal revenue.”

Fiscal stability risks

“From a cross-country perspective, China’s debt position is still comfortable. The augmented fiscal debt to GDP ratio is comparable to other emerging markets and well below that of most advanced economies. However, based on the augmented fiscal data, China has considerably less fiscal space than suggested by the general government data. Moreover, in 2012 China’s augmented fiscal deficit is larger than the general government deficit in most other emerging and advanced economies.”

“The favorable interest-growth differential has been a key factor helping keep China’s augmented debt ratio in check. As such, a reversal is one of the main risk factors for the debt outlook…Growth slowdowns—or, in our terms, a worsening of the interest-growth differential—have often been behind debt crises.”

“Debt servicing is another potential source of vulnerability. LGFVs will need some combination of cash or financing to repay maturing debt. If refinancing, LGFVs could, depending on market conditions, have to pay higher interest rates.”