Goldman Sachs Research takes another look at soaring warehouse queues and fears of price distortions in the aluminum market (see previous post here). A case can be made that inventories have risen as consequence of a supply surplus, rather than distortions. The price of physical metal, traded outside the exchange, appears to evolve in line with fundamentals. By contrast, the exchange price trades at a discount, because it only entitles to a warrant for cheapest delivery and not to physical metal at the required location. The variation of this discount constitutes basis risk for producers or consumers that use it for hedging, compromising the validity of the London Metals Exchange prices.

“The economic role of a warehouse exchange”

Goldman Sachs Commodity Research, October 31, 2013

The below are excerpts from the report. Emphasis and cursive text has been added. For access to the document please contact Goldman Sachs directly.

Metals exchanges and warehouse queues

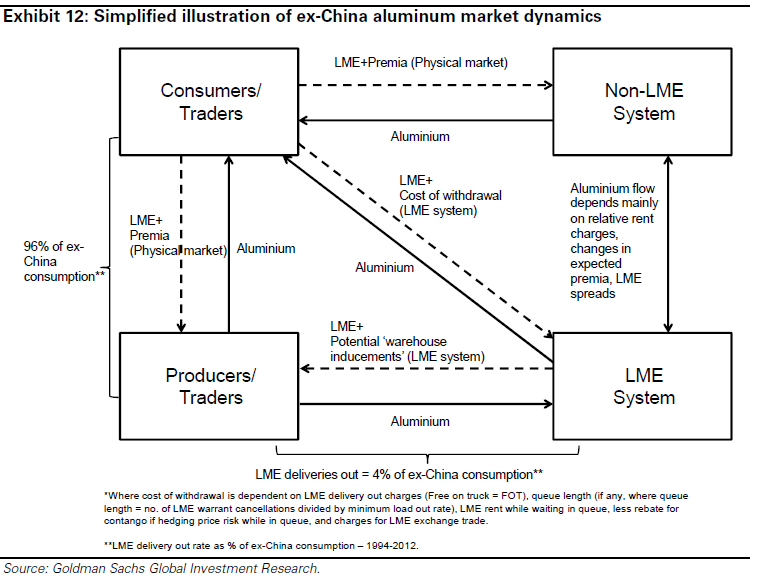

“The global aluminum market involves a variety of participants including producers, traders, financial institutions, and consumers, as well as two primary exchanges, the London Metals Exchange (LME) – which is the dominant pricing system for aluminum outside of China, and the Shanghai Futures Exchange (SHFE), which is the dominant pricing system for aluminum inside of China, and finally off-exchange warehouses.”

“For the LME markets, where like other warehouse exchange markets the exchange price does not converge to the physical price, the difference between the physical price and the exchange price is known as the physical premium. However, we believe the term ‘physical premium’ misrepresents the economic roles that the physical and exchange markets play – a better term would be ‘exchange discount’. This is because the LME prices the value of a warrant for delivery, and like any other financial warrant, as the cost of taking delivery against this warrant rises, its value will decline.”

“The main disadvantage of the current system is the volatility in basis (premia). This in turn, has increased the cost of using the LME as a hedge against physical prices – producers have faced negative basis in deficit markets while consumers have faced wide basis in large and sustained surplus markets.”

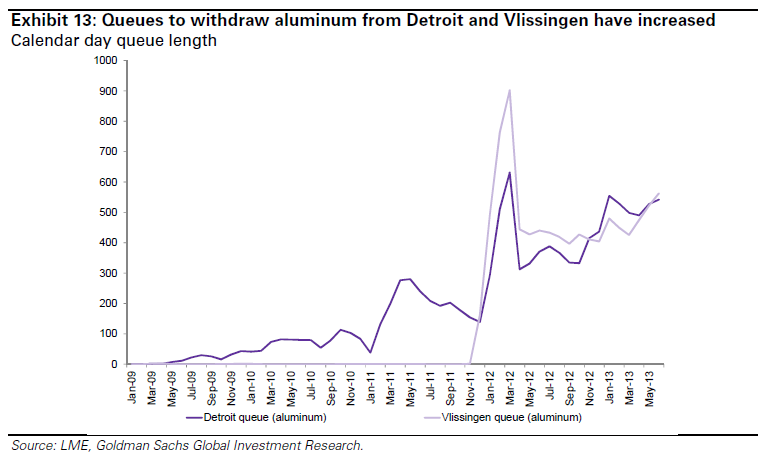

“Rising wait times for warrant withdrawal increase the cost of delivery, which, in turn, increases the ‘exchange discount’, thereby widening the spread between the physical and exchange markets. The decline in the ‘physical price’ has been composed of a falling LME price and, at the same time, rising physical premiums (premia). This, in turn, has increased the “basis” risk of using the LME as a hedge against physical prices. Specifically, the premia for aluminum have risen to record high levels – both in levels and as a percentage of price – and wait times, or the “queue”, for aluminum to be withdrawn from the Detroit and Vlissingen LME warehouse locations have risen to over a year.

The economic interpretation of aluminum prices

“The role of a physical market [for aluminum or ther base metals]…is to match buyers and sellers trading at a specified location. As a result, supply and demand fundamentals are central to determining the prices that clear these markets… For US aluminum…the Midwest transaction price that pre-dates the LME contract (1978) …is the cornerstone of nearly all US aluminum physical transactions.”

“In contrast, the role of an exchange market – such as the LME – is to promote market liquidity, fundamental transparency, risk diversification and a market of last resort during times of duress. The LME price is not the price that consumers pay for physical aluminum, but rather the value of a warrant for delivery to the cheapest warehouse anywhere in the world … In other words, the LME price does not clear aluminum supply and demand in any region, but is instead a quoting mechanism. For reference, an aluminum warrant is a document of possession, issued by the warehouse company, for each 25t lot of LME-approved aluminum metal held within an LME-approved facility. Warrants are used as the means of delivering metal under LME contracts.”

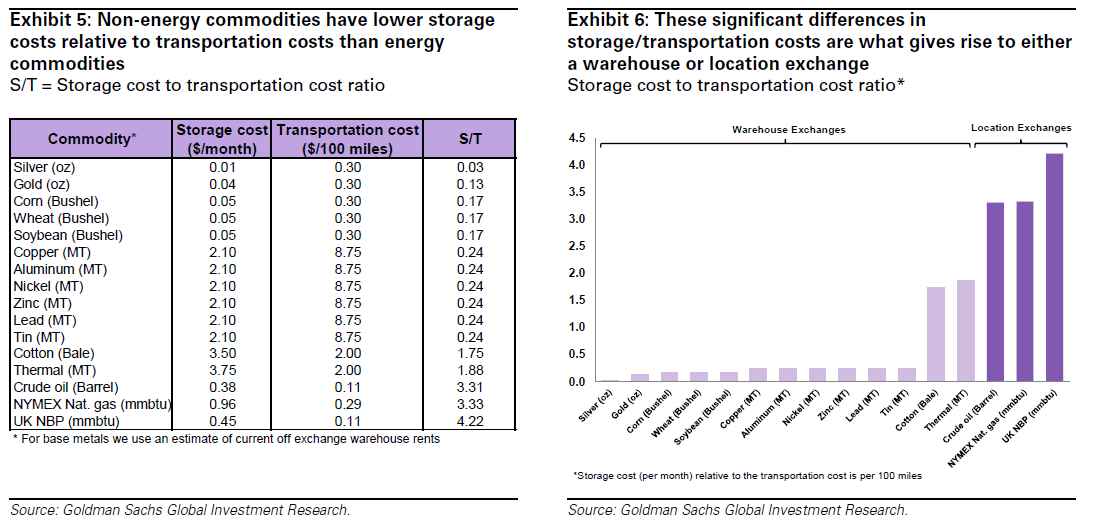

“Some exchange markets, such as energy, converge on contract expiry to physical markets, diminishing the importance of this distinction between physical and exchange; we have termed these exchanges location markets. In contrast, metals and other non-energy exchanges do not converge to physical markets at a location; we therefore refer to these exchanges as warehouse markets, where the distinction between the physical and exchange is critical. We find the cost of storage relative to the cost of transportation is the primary driver of this distinction between location and warehouse markets. When storage costs are low relative to transportation costs, as is the case for most non-energy commodities, storage and pricing is far more disperse, making centralized location markets difficult and giving rise to warehouse markets.”

Are LME queues and inventories indicative of price distortions?

“When LME warrant cancellations rise above the minimum load-out rate, a ‘queue’ for metal waiting to be delivered out of the LME warehouse location develops… there has been an unprecedented build-up of aluminum inventories in recent years, both within the LME warehousing system, as well as outside of it.”

“Aluminum is financed or carried when the physical purchase of metal is accompanied by a forward sale into the LME futures curve with the financier thereby ‘earning’ the contango in exchange for paying for the aluminum costs of carry. While all physical aluminum being financed or carried in this way could be referred to as being in a ‘financing deal’, typically ‘financing deals’ are distinguished by discounted rents– either rents are discounted by negotiation with an LME warehouse, or discounted in the sense that off-market rents are much lower than maximum LME rents, in exchange for storing the metal in a particular facility.”

“Importantly, any and all of these types of ‘financing deals’ will ultimately roll off or unwind should the market need it. The market will show it needs the metal by making the revenue for holding physical metal – the contango – smaller, and or making it negative via a backwardation. This would result in financing deals rolling off or unwinding, ‘freeing’ up physical aluminum for consumers. In this way, the common assertion that ‘financing deals’ constrain the supply of aluminum and decrease liquidity of LME warrants is not plausible as any shortage of warrants would result in a tightening in the market and a sustained backwardation, which has not occurred in recent years.”

Goldman Sachs’ critical view of planned LME reforms

“Policies aimed at reducing the queue and lowering basis risk (premium) will impact the economic role of the exchange market, but have no impact on the economic role of the physical market. Such policy shifts may reduce basis risk with the cost of reducing transparency, liquidity and impacting the ability of the LME to create a market of ‘last resort’.”

“The LME rules and potential queues do not impact the all-in physical price, which is entirely consistent with fundamental factors – total aluminum inventories in both LME and off-exchange warehouses, the pace of economic activity and the cost of producing aluminum. The LME rules do affect how the all-in physical price is split between the LME price and the premia by setting the equilibrium LME price. By affecting an LME warehouse’s ability to compete, the LME rules can affect how much aluminum is stored in LME warehouses. Given that LME warehouses report inventory levels and off-exchange warehouses do not, affecting an LME warehouse’s ability to compete can thus affect broader market transparency and exchange liquidity.”

“The only fundamental driver that the LME warehouse queues could potentially impact is the perceived availability of aluminum inventories in their storage facilities. We find that the aluminum in the queue was not demanded…The forward curve for the ‘all-in’ Midwest transaction price is in full carry, meaning that it more than pays for the cost of storage off-exchange, which is indicative that there is no demand for the metal going into storage, whether it is in the queue or not… Following the large physical surplus that accumulated post the global financial crisis, this market has been characterized by declining prices and deep contangos [12-month forward prices are above cash prices].”