Paul Mercier, principal adviser at the ECB, has summarized the basics and recent history of euro area money markets. His tale emphasizes what investors often miss. First, the ECB balance sheet and excess liquidity are poor measures of lending conditions. Second, the great financial crisis has generated a structural rise in banks’ borrowing from the Eurosystem, over and above their liquidity needs. Third, full allotment policies in conjunction with (sub-) zero deposit rates have led to large and potentially volatile excess reserve holdings.

http://www.bcl.lu/fr/publications/cahiers_etudes/92/BCLWP092.pdf

The below are extracts from the paper. Cursive text and emphasis has been added.

The money market is many markets

“The negotiation of…short term loans with maturities ranging from “overnight” (from today to tomorrow), up to several months (by convention up to 12 months, but in practice such loans are often granted for very short maturities up to one month), between financial institutions, takes place on the money market.”

“In reality various forms [of money market lending] coexist: unsecured bank loans (the lender has no other guarantee than the word of the borrower), repurchase agreements (the borrower sells a financial assets, and promises to re-purchase it at the term of the operation), lending guaranteed by a pledge and many others… banks could become extremely reluctant to grant loans, even for a very short period, to other banks.”

The central bank is the dominant intermediary

“The central bank acts as an intermediary between the banks running a liquidity surplus and those facing a liquidity deficit… Some banks will use the money market while others will make recourse to the central bank. The choice between the two avenues will be influenced by risks considerations…by the relative prices and, possibly more forcefully in a crisis, by rationing. Depositing with and borrowing from the central banks may be quite unattractive in financial terms but they are…not rationed.”

“The size of the central bank operations, in particular the volume of deposits it receives does not tell anything about the credit granted to the economy by the banking sector. It is just a measure of the intermediation of the central bank. Acting as an intermediary, substituting the money market to settle the imbalances between banks…[means that] both sides of its balance sheet increase as long as banks prefer avoiding transacting on the money market.”

The money market is not normally in equilibrium

“For the entire banking system a structural liquidity deficit appears…because of two factors in particular: the demand for banknotes by the public at large, and the imposition of reserve requirements by the central bank.

- The demand for banknotes by the public leads the banks to borrow, necessarily, from the central bank…a bank will maintain the stock of banknotes they hold at a minimum necessary to face immediate withdrawal by clients, and will adapt their purchases to the clients demand.

- Banks can be requested to maintain deposits with the central bank, in the form of current accounts…usually called ‘mandatory reserves‘… Being obliged to build up its current account with the central bank for the sake of fulfilling its reserve obligations, [the commercial banking system]…faces an additional liquidity deficit.”

“It is precisely in this respect that the central bank acts as the lender of last resort. The banking sector cannot find any other lender than the central bank to face its liquidity deficit.”

Money market activity increases banks’ balance sheets

“In a large banking sector, some banks do not borrow directly from the central bank, but rely on other banks that indeed borrow from the central bank more than what they actually need, using the surplus to grant money market loans to the former ones.”

“The intermediation between the central bank [and commercial banks] “inflates” [the intermediating commercial bank’s] balance sheet, as its money market loans are growing….two banks can indeed both provide credit and borrow to and from each other, because each individual transaction takes place at different moments, for different maturities, at different conditions. In addition, [since banks may belong to different types or groups]…it is again quite intuitive to understand that some banks in one group receive a loan from some other banks in the other group and vice-versa.”

“Incidentally, the consolidated balance sheet of the banking sector is not affected by interbank loans as they net out.”

Central banks influence excess liquidity

“There are circumstances in which the liquidity provided to the banking sector can exceed its actual liquidity deficit. One of them relates to the deliberate decision of the central bank…to lend more than strictly necessary.”

“Depending on the institutional set up, the central bank may want to avoid such an “excess reserves” situation and discourage it, for instance by not remunerating the amount deposited in excess of the requirement, which is the practice of the Eurosystem. However the central bank may offer a ‘deposit facility’, where banks can indeed park their excess reserves. The Eurosystem indeed makes such a deposit facility available to the banking system.”

“When the central bank provides credit in excess of the exact ‘net liquidity deficit’ of the banking sector, not only the liquidity injection increases but the recourse to the deposit facility increases at the same time… An increase of the deposit facility does not provide any information about the credit activity of banks.”

Commercial banks influence excess liquidity as well

“If the central bank decides to inject more liquidity than strictly necessary, some recourse to the deposit facility will occur. However, a second reason explaining the recourse to the deposit facility resides in the preference of banks for not lending to other banks on the money market. This is the situation observed in the euro area since 2007… In addition the central bank can decide to allow banks to borrow without limit… as the Eurosystem does since autumn 2008.”

“Assuming that the money market comes to a standstill…the cash-rich banks will find no other usage for their excess liquidity than making use of the deposit facility.”

“The absence of money market transactions leads to a greater recourse to the central bank on both sides of its balance sheet…but the net liquidity injection remains unchanged… A given net liquidity injection can take place with a central bank provision of credit equal to the net liquidity deficit of the banking sector, or by a greater provision of credit compensated by the use of the deposit facility by banks.”

Money markets can fragment

“Considering the entire banking sector on its whole one could be inclined to conclude that they are banks borrowing some ‘liquidity’ from the central bank just to re-deposit it with the same central bank, but the reality is quite different. Notwithstanding a slight overlap between the two populations of borrowers and depositors, a number of banks (belonging to the population of cash-poor institutions) borrow from the central bank to cover their liquidity needs, not having access anymore to the money market. Symmetrically other banks (qualified as cash-rich) prefer depositing their excess liquidity with the central bank rather than lending it to the first group of banks.”

The Eurosystem balance sheet explains the state of the money market

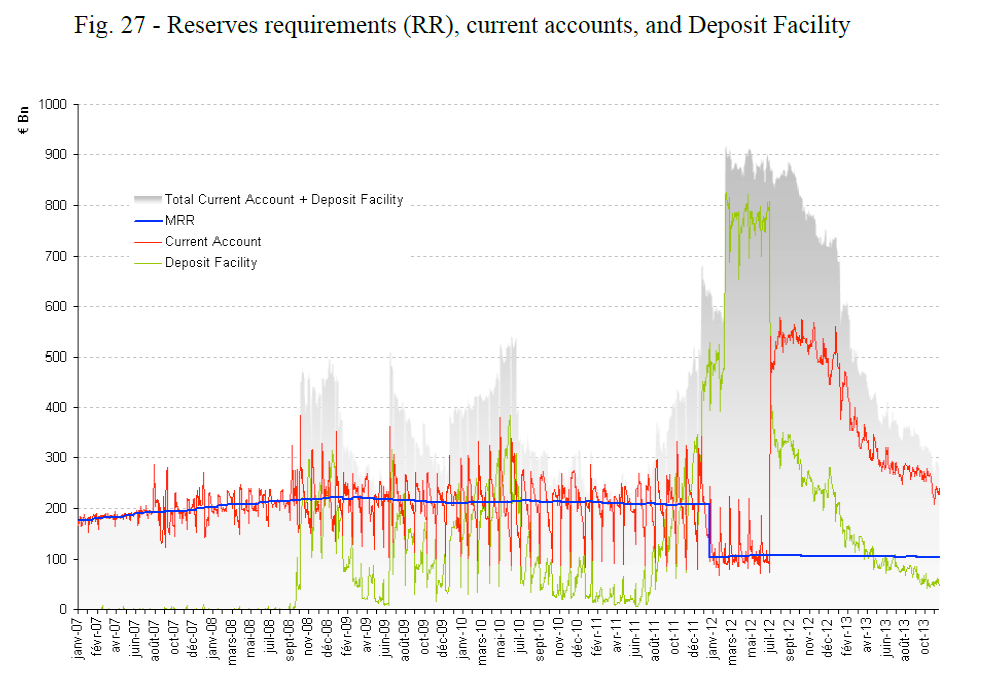

“[In] the Eurosystem…the use of the deposit facility has evolved in quite a spectacular way, reflecting the malfunctioning of the money market.”

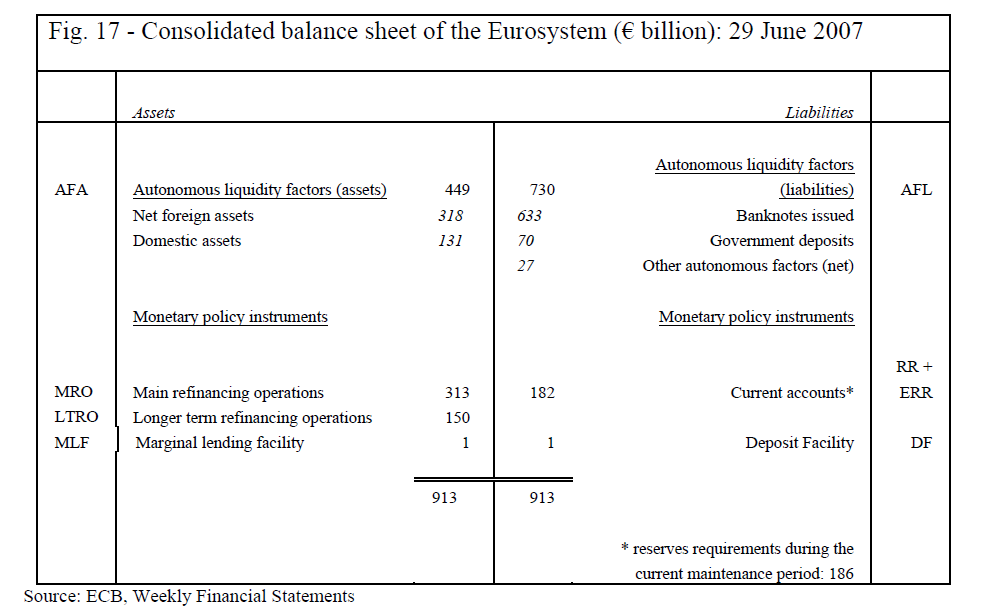

“The need to borrow from the central bank, designated…as net liquidity deficit of the banking sector, correspond to the net value of the autonomous factors [AFL – AFA on the consolidated Eurosystem balance sheet, as per below], plus the reserves requirements [RR]. This need is ‘financed’ by the recourse to the different monetary policy instruments offered by the Eurosystem.”

“The banking sector has to borrow that amount by using any of the monetary policy instruments used by the Eurosystem: the main refinancing operations (MRO), the longer term refinancing operations (LTRO), or the Marginal Lending Facility (MLF). If the banks were to borrow more than necessary, the excess liquidity could remain deposited on the current accounts held for the sake of reserves requirements. However individual banks would then run the risk that at the end of the maintenance period their average deposit exceeds their requirement in which case the excess is not remunerated. To avoid such a loss of remuneration, banks prefer using the Deposit Facility.”

Net borrowing just covers liquidity deficit; gross borrowing determines excess liquidity

“The notion of net borrowing is useful. It makes explicit that the banking sector indeed borrows from the Eurosystem through the different types of operations (MRO, LTRO, and MLF), let us call this the gross borrowing. Yet the banking sector, as a whole, may simultaneously lend to the central bank by maintaining deposits on the current accounts in excess of the required reserves (ERR) or on the deposit facility (DF)… the net borrowing of the banking sector is necessary equal to its liquidity deficit…The notion of “excess liquidity” simply refers to a situation where the gross borrowing of the banking sector is larger than the actual liquidity deficit, leading either to the accumulation of excess reserves or recourse to the deposit facility.”

Prior to the subprime crisis money markets worked efficiently

“In June 2007, banks accessing the Eurosystem borrowed an amount equivalent to the net liquidity deficit of the whole banking sector…his simply means that the banks participating in the operations of the Eurosystem borrowed what the entire banking sector needed while the money market ‘took care’ of the redistribution. At that time a group of 800 banks, out of a population of more than 6.500, actually participated in the monetary policy operations…The recourse to both standing facilities (marginal lending facility and deposit facility) was very limited in size. In practice, it was only for technical reasons, and more particularly on the last day of a given maintenance period, that this occurred.”

Crisis-driven market changes required gross borrowing well above the net liquidity deficit

“One characteristic of the financial crisis…was that…banks became and still are quite reluctant to lend to each other. In 2008 the Governing Council of the ECB took an exceptional decision. As indicated earlier, since 1999 the Eurosystem had controlled the quantity of liquidity to inject into the banking sector. In October 2008 the Governing Council decided to leave to the banking sector itself the choice of the quantity of liquidity to be injected through monetary policy operations. Indeed it decided that all its allocations of credit, for all maturities, 1-week, 1-month24, three-month, six-month, and later-on 1-year and 3-year operations will be based on a fixed rate with full allotment. From then onwards the banking sector decides itself how much liquidity it acquires from the Eurosystem.”

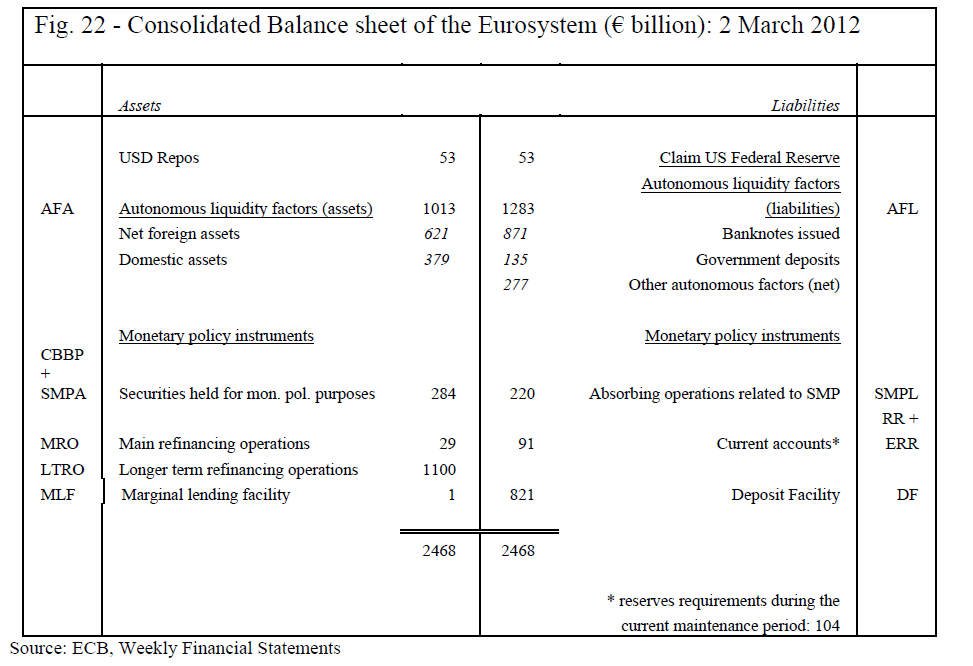

“It is striking to observe that the net liquidity deficit of the banking sector in June 2007 and September 2011 are very similar: 467 and 454 bn respectively. Indeed, the composition of the autonomous factors has evolved but, for instance, the movements in other autonomous factors compensated an increase of banknotes in circulation from 633 to 857 bn. Therefore the net borrowing by the banking sector is equal to the amount of 454 bn. However the gross borrowing is much larger, reaching 651 bn, compensated by a large recourse to the deposit facility.”

“The introduction of a second 3-year LTRO, shaped the Eurosystem balance sheet further… in particular the share of the MRO has been reduced substantially, while the LTRO outstanding amounts have increased further (even if some substitution took place, within that category, between credits with a 3-month or a 6-month maturity and the recourse to the 3-year LTRO).”

Zero (and negative) deposit rates boost excess reserves

“Banks normally have no interest in maintaining excess reserves on their current account as the required reserves only are remunerated. Banks facing an excess liquidity will use the deposit facility instead, because it usually offers some remuneration, even if rather low. However when the rate of the deposit facility doesn’t offer a remuneration any longer, banks are indifferent between keeping funds in excess reserves on the current account and making recourse to the deposit facility.”

“The sole observation of the deposit facility would provide a wrong measure of the excess liquidity, which cannot be appreciated without taking into account the level of reserves requirements and the use of the current accounts for parking part of the excess liquidity in the form of excess reserves.”